Business loan application process sets the stage for entrepreneurs seeking financial support, unraveling the intricate steps and requirements for securing vital funding. Dive into this detailed guide to navigate the complexities of loan applications with confidence.

Explore the nuances of different loan types, understand the significance of meticulous preparation, and unravel the decision-making processes of lenders in this comprehensive exploration of business loan applications.

Overview of Business Loan Application Process

When applying for a business loan, there are typical steps involved that are crucial to securing the financing needed. Understanding these steps and the key documents required can help streamline the application process and increase the chances of approval.

Steps in Business Loan Application

- Research and Preparation: Before applying for a business loan, it is essential to research different lenders and loan options to find the best fit for your business. Prepare all necessary documents, including financial statements, business plans, and credit reports.

- Application Submission: Once you have selected a lender, complete the loan application form accurately and submit it along with the required documents. Be sure to provide all requested information to avoid delays in processing.

- Review and Underwriting: The lender will review your application and documents to assess your creditworthiness and the viability of your business. This may involve a detailed analysis of your financials and business plan.

- Loan Approval or Rejection: Based on the review process, the lender will either approve or reject your loan application. If approved, you will receive a loan offer outlining the terms and conditions of the financing.

- Acceptance and Funding: If you agree to the terms of the loan offer, you can accept it and proceed to the funding stage. The lender will disburse the funds to your business account, usually within a few days.

Key Documents Required

- Business Plan: A detailed business plan outlining your business goals, financial projections, and market analysis is crucial for demonstrating the viability of your business.

- Financial Statements: Current financial statements, including profit and loss statements, balance sheets, and cash flow statements, provide a snapshot of your business’s financial health.

- Tax Returns: Personal and business tax returns for the past few years help lenders assess your income and financial history.

- Credit Reports: Both personal and business credit reports are typically required to evaluate your creditworthiness and repayment ability.

- Legal Documents: Any relevant legal documents, such as business licenses, contracts, or leases, may be needed to verify the legitimacy of your business.

Importance of Each Step

- Research and Preparation: Proper research and preparation ensure that you approach the right lenders and have all necessary documents ready, increasing your chances of approval.

- Application Submission: Submitting a complete and accurate application helps expedite the review process and demonstrates your professionalism to the lender.

- Review and Underwriting: Thorough review and underwriting ensure that the lender assesses your financial situation and business viability accurately, leading to informed decisions on loan approval.

- Loan Approval or Rejection: Transparent communication on loan approval status helps you plan your next steps accordingly, whether exploring other financing options or proceeding with the approved loan offer.

- Acceptance and Funding: Prompt acceptance of a loan offer and proper utilization of the funds can support your business’s growth and operational needs effectively.

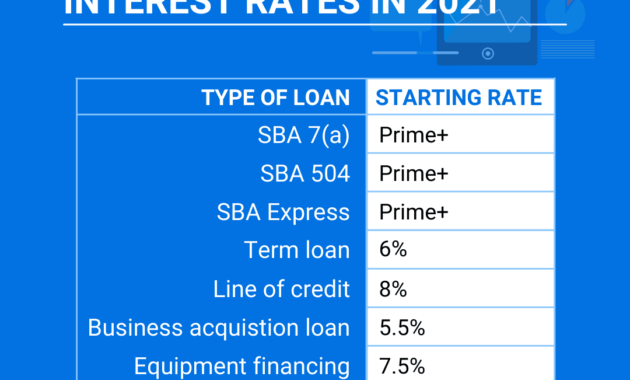

Types of Business Loans

Business loans are essential for funding various business needs, and different types of loans cater to specific requirements. Understanding the types of business loans available in the market can help businesses make informed decisions when seeking financial assistance.

Term Loans

Term loans are a common type of business loan where a lump sum is borrowed and repaid over a set period with fixed payments. These loans can be short-term or long-term, with varying repayment terms and interest rates. Eligibility criteria often include a good credit score, business financials, and collateral for security.

Lines of Credit

A line of credit provides businesses with access to a predetermined amount of funds that can be drawn upon as needed. Interest is only charged on the amount borrowed, making it a flexible financing option. Eligibility requirements typically include a strong credit history, business revenue, and financial stability.

SBA Loans

Small Business Administration (SBA) loans are government-backed loans designed to support small businesses. These loans offer competitive interest rates and longer repayment terms. Eligibility criteria include meeting SBA size standards, demonstrating the need for financial assistance, and having a solid business plan.

Equipment Financing

Equipment financing allows businesses to purchase or lease equipment by using the equipment itself as collateral. The loan term is usually aligned with the equipment’s useful life. Eligibility requirements may include the equipment’s value, business financials, and creditworthiness.

Secured vs. Unsecured Loans

Secured business loans require collateral, such as business assets or personal guarantees, to secure the loan. Unsecured loans, on the other hand, do not require collateral but may have higher interest rates. Secured loans offer lower interest rates and higher loan amounts, while unsecured loans are suitable for businesses without valuable assets to pledge.

When looking to purchase a new car, getting pre-approved auto loans can save you time and money. By having your financing secured beforehand, you can negotiate better deals with car dealerships. Pre-approved auto loans also give you a clear idea of your budget, preventing you from overspending. To learn more about the benefits of pre-approved auto loans, visit Pre-approved auto loans.

Preparing for a Business Loan Application

Before embarking on the business loan application process, there are several important tasks that need to be completed to increase your chances of success. One of the key elements is having a solid business plan in place, as well as ensuring your credit score and financial statements are in order.

Checklist of Tasks

- Review and organize your financial documents, including tax returns, bank statements, and financial statements.

- Check your credit score and address any issues that may negatively impact your application.

- Create a detailed business plan outlining your company’s mission, goals, target market, and financial projections.

- Determine the amount of funding you need and how it will be used within your business.

- Research and compare different lenders to find the best fit for your business needs.

Importance of a Solid Business Plan

A well-thought-out business plan is crucial for a successful loan application as it demonstrates to lenders that you have a clear vision for your business and a strategic roadmap for achieving your goals. It also helps you identify potential risks and challenges, allowing you to proactively address them before they become obstacles to securing funding.

Impact of Credit Scores and Financial Statements, Business loan application process

Your credit score and financial statements play a significant role in the loan application process. Lenders use this information to assess your creditworthiness and determine the risk associated with lending to your business. A high credit score and healthy financial statements can increase your chances of approval and may also help you secure better loan terms, such as lower interest rates or higher loan amounts.

Submitting the Application

When submitting a business loan application, it is crucial to provide accurate and complete information to increase the chances of approval. Lenders rely on the information provided to assess the creditworthiness and viability of the business. Incomplete or inaccurate information can lead to delays or even rejection of the application.

Information Required in a Business Loan Application Form

- Business details such as name, address, type of business, and industry.

- Financial information including revenue, profit and loss statements, balance sheets, and cash flow projections.

- Personal information of the business owner such as credit history, assets, liabilities, and income.

- Purpose of the loan and how the funds will be used.

Significance of Providing Accurate and Complete Information

- Accurate information helps lenders make informed decisions about the loan application.

- Complete information ensures transparency and builds trust with the lender.

- Inaccurate or incomplete information can lead to delays in the approval process.

- Providing all required information upfront can expedite the loan approval process.

Submitting the Application and Associated Fees

- Once the application form is completed, it can be submitted online, in person, or through a designated channel provided by the lender.

- Some lenders may charge an application or processing fee, which should be disclosed upfront.

- It is important to review all terms and conditions related to the application process, including any associated fees.

- Submitting the application in a timely manner and following up with the lender can help expedite the approval process.

Review and Approval Process

After submitting a business loan application, the review and approval process begins. Lenders carefully evaluate the application to assess the creditworthiness of the borrower and the viability of the business.

Evaluation Criteria

When evaluating loan applications, lenders typically consider factors such as the borrower’s credit score, business financials, cash flow, collateral, and business plan. They look for evidence that the business is profitable, has the ability to repay the loan, and poses minimal risk.

When it comes to purchasing a new car, having a pre-approved auto loan can make the process much smoother. By getting pre-approved for a loan, you’ll know exactly how much you can afford to spend, which can help you narrow down your options and negotiate with confidence. Check out this helpful guide on pre-approved auto loans to learn more about the benefits and how to get started.

- Credit Score: A high credit score indicates a history of responsible credit management and increases the chances of loan approval.

- Business Financials: Lenders review financial statements, tax returns, and bank statements to assess the financial health of the business.

- Cash Flow: Positive cash flow demonstrates the ability to generate enough revenue to cover expenses and repay the loan.

- Collateral: Providing collateral can reduce the lender’s risk and improve the chances of approval.

- Business Plan: A well-developed business plan Artikels the company’s goals, operations, and financial projections, showing the lender that the business is well-managed and has a clear strategy for success.

Common Reasons for Rejection

There are several common reasons why a business loan application may be rejected. These include:

- Insufficient Credit History: Limited or poor credit history may make it difficult for lenders to assess the borrower’s creditworthiness.

- Poor Financials: Weak financial performance, low cash flow, or high debt levels can signal financial instability and increase the risk of default.

- Lack of Collateral: Without adequate collateral to secure the loan, lenders may be reluctant to approve the application.

- Incomplete or Inaccurate Documentation: Missing or inaccurate information in the application can raise red flags and lead to rejection.

- High Risk Industry: Some industries are considered higher risk by lenders, making it harder to secure financing.

Concluding Remarks

Embark on your loan application journey armed with knowledge and insights from this guide, ensuring a smoother path towards securing financial support for your business endeavors.

FAQ Insights

What are the key documents required during a business loan application?

The key documents typically required include financial statements, business plans, tax returns, and personal identification.

How do credit scores impact the loan application process?

Credit scores play a crucial role in determining loan approval and interest rates, showcasing the borrower’s creditworthiness to lenders.

What are the common reasons for loan application rejection?

Common reasons include poor credit history, inadequate collateral, insufficient cash flow, and incomplete or inaccurate information provided in the application.