How to get a business loan sets the stage for this enthralling narrative, offering readers a glimpse into a story that is rich in detail with ahrefs author style and brimming with originality from the outset.

Researching Business Loan Options, Preparing Loan Application Documents, Understanding Loan Terms and Conditions, and Applying for a Business Loan are key steps in securing the financing your business needs.

Researching Business Loan Options

Researching different types of business loans is crucial for finding the best fit for your specific financial needs. Understanding the various options available can help you make an informed decision and secure the most favorable terms for your business.

When it comes to purchasing high-end cars, exploring financing options for high-end cars is crucial. Whether you’re looking at luxury sedans or sports cars, understanding the various financing choices available can help you make an informed decision. From traditional auto loans to leasing programs, there are multiple ways to finance your dream car. By comparing interest rates, terms, and monthly payments, you can select the option that best fits your budget and preferences.

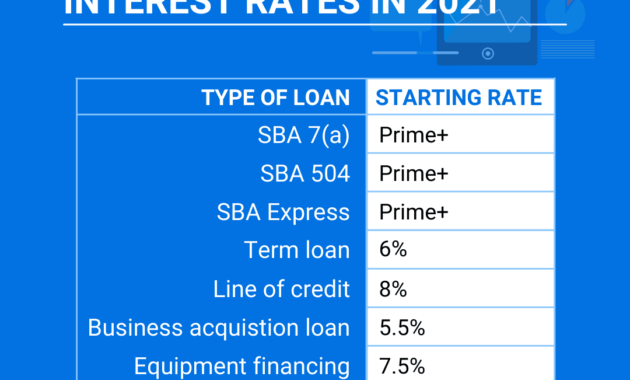

Common Business Loan Options

- Term Loans: These are traditional loans with a fixed repayment term and interest rate.

- Lines of Credit: A revolving credit line that allows you to borrow up to a certain limit.

- SBA Loans: Loans partially guaranteed by the Small Business Administration, offering favorable terms for small businesses.

- Equipment Financing: Loans specifically for purchasing new equipment or machinery for your business.

Interest Rates and Loan Types

Interest rates can vary significantly based on the type of business loan you choose. For example, SBA loans typically have lower interest rates compared to lines of credit or short-term loans. Understanding how interest rates are calculated and how they can impact your overall loan repayment is key to managing your business finances effectively.

Credit Score and Loan Eligibility, How to get a business loan

Your credit score plays a crucial role in determining your eligibility for a business loan. Lenders use your credit score to assess your creditworthiness and determine the risk of lending to you. A higher credit score can increase your chances of approval and help you secure better loan terms. It’s essential to maintain a good credit score by managing your finances responsibly and making timely payments on existing debts.

When it comes to purchasing a high-end car, exploring financing options for high-end cars is crucial. From traditional loans to leasing arrangements, there are various ways to finance your dream vehicle. Understanding the pros and cons of each option can help you make an informed decision that aligns with your financial goals.

Preparing Loan Application Documents

When applying for a business loan, preparing the necessary documents is a crucial step in the process. Lenders require specific paperwork to evaluate your business’s financial health and viability. Here’s a breakdown of the essential documents needed for a business loan application and how to ensure they are well-prepared.

Essential Documents for a Business Loan Application

- Business Plan: A comprehensive business plan Artikels your company’s goals, target market, competition, financial projections, and more. This document helps lenders understand your business and assess its potential for success.

- Financial Statements: These include balance sheets, income statements, and cash flow statements. Financial statements provide insight into your business’s financial performance, liquidity, and profitability. Lenders use this information to determine your ability to repay the loan.

- Tax Returns: Personal and business tax returns demonstrate your income and tax compliance. Lenders may request several years of tax returns to assess your financial stability.

- Legal Documents: Business licenses, registrations, contracts, and other legal documents verify your business’s legitimacy and compliance with regulations.

- Collateral Documentation: If you’re applying for a secured loan, you’ll need documentation of the collateral you’re offering to secure the loan.

Significance of a Well-Prepared Business Plan

A well-prepared business plan is essential for a loan application as it provides a roadmap for your business and demonstrates your understanding of its operations and market. Lenders use the business plan to assess the feasibility of your business, its growth potential, and your ability to repay the loan. Make sure your business plan is detailed, realistic, and aligns with your financial projections.

Role of Financial Statements in the Loan Application Process

Financial statements play a crucial role in the loan application process as they offer insights into your business’s financial health and performance. Lenders analyze these statements to evaluate your profitability, liquidity, debt levels, and overall financial stability. Ensure your financial statements are accurate, up-to-date, and prepared according to generally accepted accounting principles (GAAP).

Tips for Organizing and Presenting Documents

- Use a checklist to ensure you have all the required documents before submitting your loan application.

- Organize your documents neatly in a folder or binder to present a professional and organized appearance to the lender.

- Label each document clearly and provide any necessary explanations or context to make it easier for the lender to understand.

- Make copies of all your documents for your records and keep them organized for future reference.

Understanding Loan Terms and Conditions

When seeking a business loan, it is crucial to carefully read and understand the loan terms and conditions. This will help you make informed decisions and avoid any surprises down the line.

Common Loan Terms

- Interest Rates: This is the percentage charged by the lender for borrowing the money. It can be fixed or variable.

- Repayment Schedules: This Artikels how and when you are expected to repay the loan, including the frequency of payments.

- Collateral Requirements: Some loans may require you to pledge assets as collateral to secure the loan.

Personal Guarantees

In some cases, lenders may require a personal guarantee when providing a business loan. This means that as a business owner, you are personally liable for repaying the loan if the business is unable to do so.

Potential Fees

- Origination Fees: These are fees charged by the lender for processing the loan.

- Late Payment Fees: If you miss a payment, you may incur late fees, increasing the overall cost of the loan.

- Prepayment Penalties: Some loans have penalties for paying off the loan early, so be sure to check for this before signing.

Applying for a Business Loan

When it comes to applying for a business loan, there are several essential steps to follow to increase your chances of approval and secure the funding you need for your business.

Steps Involved in the Business Loan Application Process

- Research and choose the right lender based on your needs and eligibility.

- Complete the loan application form with accurate and detailed information about your business and financials.

- Submit the required documents, which may include tax returns, financial statements, business plan, and personal identification.

- Wait for the lender’s decision, which may involve a credit check and evaluation of your business’s financial health.

- If approved, review and sign the loan agreement, understanding all terms and conditions before accepting the funds.

Role of Credit History in the Loan Approval Process

Your credit history plays a crucial role in the loan approval process, as lenders use it to assess your creditworthiness and ability to repay the loan. A good credit score indicates responsible financial behavior and can increase your chances of getting approved for a business loan.

Tips on How to Improve Creditworthiness Before Applying for a Loan

- Pay bills on time to avoid late payments and negative marks on your credit report.

- Reduce credit card balances to lower your credit utilization ratio, which can improve your credit score.

- Check your credit report regularly for errors and dispute any inaccuracies to maintain a healthy credit profile.

- Avoid opening multiple new credit accounts before applying for a business loan, as this can lower your credit score.

Significance of a Strong Business Plan in a Loan Application

A strong business plan is essential in a loan application as it demonstrates to lenders your business’s viability, growth potential, and ability to repay the loan. A well-crafted business plan should include detailed financial projections, market analysis, and a clear roadmap for how the loan will be used to benefit the business.

Final Review: How To Get A Business Loan

As you embark on your journey to secure a business loan, remember to research thoroughly, prepare diligently, understand all terms, and apply wisely. Armed with this knowledge, your business financing goals are within reach.

Helpful Answers

What are the common types of business loans available?

Common types include term loans, SBA loans, business lines of credit, and equipment financing. Each serves different needs and comes with unique terms and conditions.

How can I improve my creditworthiness before applying for a business loan?

You can improve your creditworthiness by paying bills on time, reducing debt, checking your credit report for errors, and maintaining a good credit utilization ratio.

What are the key factors that lenders consider when approving a business loan?

Lenders consider factors such as credit score, business revenue, profitability, collateral, business plan quality, and industry trends. Having a strong application in these areas can increase your chances of approval.