Kicking off with First-time car buyer loan, this opening paragraph is designed to captivate and engage the readers, setting the tone ahrefs author style that unfolds with each word.

First-time car buyer loans are specifically tailored for individuals stepping into the world of car ownership for the first time. This guide will walk you through everything you need to know about securing your dream car with your limited credit history.

Introduction to First-time Car Buyer Loan

A first-time car buyer loan is a specialized type of loan designed for individuals who are purchasing a vehicle for the first time. These loans are tailored to meet the needs of individuals with limited or no credit history, making it easier for them to secure financing for their first car.

Why First-time Car Buyer Loans are Different

First-time car buyer loans differ from regular car loans in that they are specifically structured to accommodate borrowers with limited credit history. Lenders offering these loans understand the challenges faced by first-time buyers and provide more flexible terms and conditions to help them get approved.

The Importance of First-time Car Buyer Loans

First-time car buyer loans play a crucial role in enabling individuals with limited credit history to purchase their first vehicle. These loans provide an opportunity for new borrowers to establish a positive credit history by making timely payments, which can benefit them in future financial endeavors.

Eligibility Criteria

First-time car buyer loans typically have specific eligibility requirements that individuals need to meet in order to qualify for the loan. These criteria are designed to ensure that the borrower has the financial capacity to repay the loan and to minimize the risk for the lender.

Typical Eligibility Requirements, First-time car buyer loan

- A minimum credit score: Lenders may require a minimum credit score to qualify for a first-time car buyer loan. This score is used to assess the borrower’s creditworthiness and ability to repay the loan.

- Proof of income: Borrowers are usually required to provide proof of income, such as pay stubs or tax returns, to demonstrate their ability to make monthly loan payments.

- Down payment: Some lenders may require a down payment to secure the loan. This helps reduce the amount of money borrowed and shows the borrower’s commitment to the purchase.

- Valid driver’s license: Borrowers are typically required to have a valid driver’s license to qualify for a first-time car buyer loan. This is necessary to legally operate the vehicle being purchased.

Documents Required

- Proof of identity: Borrowers will need to provide a valid form of identification, such as a driver’s license or passport, to verify their identity.

- Proof of residence: Lenders may require proof of residence, such as a utility bill or lease agreement, to confirm the borrower’s current address.

- Vehicle information: Borrowers may need to provide details about the vehicle they intend to purchase, including VIN number, make, model, and year.

- Employment information: Lenders may request details about the borrower’s employment status, including employer contact information and length of employment.

Loan Options and Terms

When it comes to first-time car buyer loans, there are several options available in the market to suit different financial situations and needs. Understanding the types of loans, interest rates, and terms offered by various lenders can help you make an informed decision when purchasing your first car.

Calculating your monthly car payments can be a breeze with the help of a reliable car loan calculator. By entering the loan amount, interest rate, and term, you can quickly determine how much you’ll need to budget for your new vehicle. This handy tool takes the guesswork out of financing and allows you to make informed decisions when shopping for your dream car.

Types of First-Time Car Buyer Loans

- Traditional Auto Loans: These loans are offered by banks, credit unions, and online lenders. They typically have fixed interest rates and require a down payment.

- Manufacturer Financing: Car manufacturers often provide financing options through their dealerships. These loans may come with special incentives or promotional rates.

- Bad Credit Car Loans: Designed for individuals with less-than-perfect credit, these loans usually have higher interest rates to compensate for the higher risk.

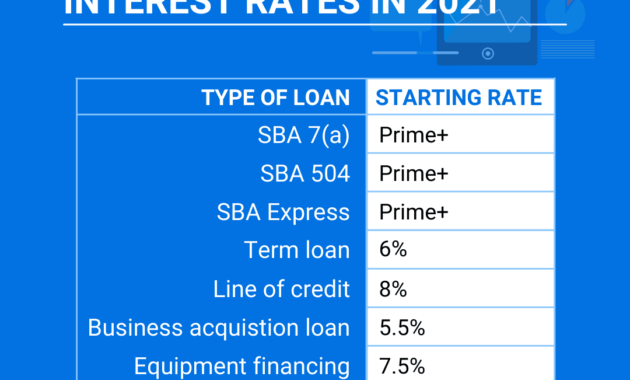

Interest Rates for First-Time Buyers

- Interest rates for first-time car buyers can vary depending on the lender, your credit score, and the loan term. On average, first-time buyers can expect to pay interest rates ranging from 4% to 20%.

- Individuals with good credit scores are more likely to qualify for lower interest rates, while those with poor credit may face higher rates.

Terms and Conditions of Lenders

- Loan Amount: Lenders may have minimum and maximum loan amounts for first-time car buyers.

- Loan Term: The length of the loan term can vary, with typical terms ranging from 36 to 72 months. Longer loan terms may result in lower monthly payments but higher overall interest costs.

- Down Payment: Some lenders may require a down payment for first-time car buyer loans, while others may offer 100% financing.

- Fees: Be aware of any additional fees associated with the loan, such as origination fees, prepayment penalties, or late payment fees.

Building Credit History

Building a solid credit history is crucial for financial stability and future loan approvals. First-time car buyers can use these loans as a stepping stone towards establishing a positive credit profile.

When considering buying a new car, it’s essential to calculate your finances beforehand. Using a car loan calculator can help you estimate monthly payments based on interest rates and loan terms. By inputting the purchase price and down payment, you can determine a budget that suits your financial situation. This tool is valuable in making informed decisions and ensuring you can afford the vehicle you desire.

Utilize Loans Responsibly

One effective way to build credit history is by making timely payments on your first-time car buyer loan. By consistently paying off your monthly installments on time, you demonstrate to lenders that you are a responsible borrower.

Monitor Credit Score

Regularly monitoring your credit score can also help you track your progress in building credit history. You can access your credit report from major credit bureaus and identify areas for improvement.

Long-Term Benefits

Responsible management of a first-time car buyer loan can lead to long-term benefits such as lower interest rates on future loans, increased credit limits, and better loan terms. By establishing a positive credit history early on, you set yourself up for financial success in the future.

Budgeting and Affordability: First-time Car Buyer Loan

When it comes to purchasing a car for the first time, budgeting is a crucial aspect to consider. It’s essential to determine how much you can afford to spend on a loan while also factoring in additional costs associated with car ownership.

Determining an Affordable Loan Amount

Before applying for a car loan as a first-time buyer, it’s important to assess your financial situation. Calculate your monthly income, expenses, and savings to determine how much you can comfortably allocate towards a car loan payment each month. Consider using online loan calculators to estimate the monthly payments based on different loan amounts and interest rates.

Factoring in Additional Costs

- Insurance: Don’t forget to include the cost of auto insurance in your budget. Insurance premiums can vary based on factors like your age, driving record, and the type of car you purchase.

- Maintenance: Cars require regular maintenance, such as oil changes, tire rotations, and brake inspections. Budget for these ongoing expenses to keep your car in good condition.

- Registration Fees: When purchasing a car, you’ll need to pay for registration and licensing fees. These costs can vary by state, so it’s important to research the fees in your area.

Creating a Budget

To help first-time buyers create a budget for their car purchase, consider using budgeting tools and methods such as:

- Online Budget Calculators: Websites and apps offer budget calculators that can help you track your income and expenses to determine how much you can afford to spend on a car.

- Financial Advisors: Consulting with a financial advisor can provide personalized advice on budgeting for a car purchase and managing other financial goals.

- Budgeting Apps: Utilize budgeting apps that allow you to set spending limits, track expenses, and save towards your car purchase goal.

Last Recap

As we conclude this guide on first-time car buyer loans, remember that taking this step not only gets you on the road but also helps you establish a solid credit history for your financial future. With the right knowledge and tools, you can confidently make your first car purchase a reality.

FAQ Explained

What documents are typically required to apply for a first-time car buyer loan?

Documents like proof of income, identification, and residence are commonly needed to apply for a first-time car buyer loan.

Can first-time car buyer loans help improve credit scores?

Yes, by making timely payments on the loan, first-time car buyers can gradually improve their credit scores over time.

How can first-time buyers determine an affordable loan amount?

First-time buyers can assess their monthly budget, including additional costs like insurance and maintenance, to determine an affordable loan amount.